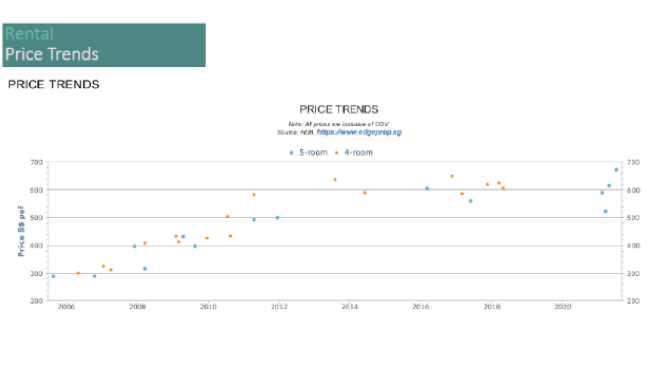

With Rising Inflation rates, the occurrence where the older folks are getting caught off guard and finding themselves without sufficient cash to meet even daily necessities is becoming painfully common.

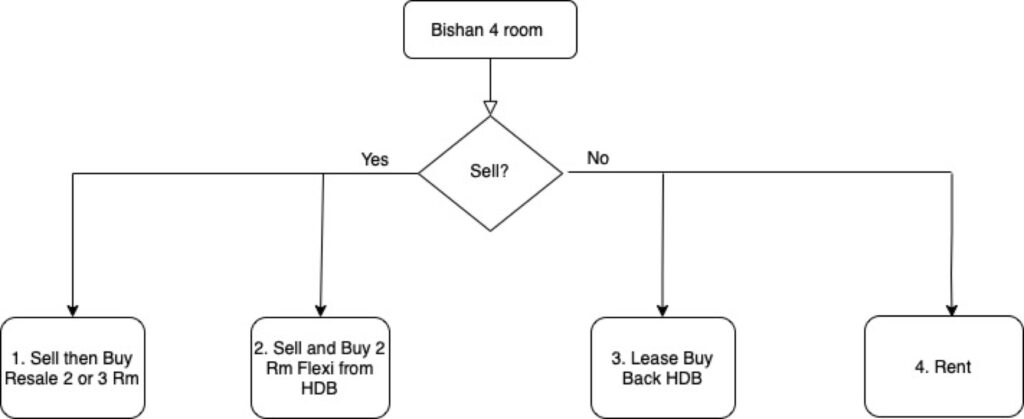

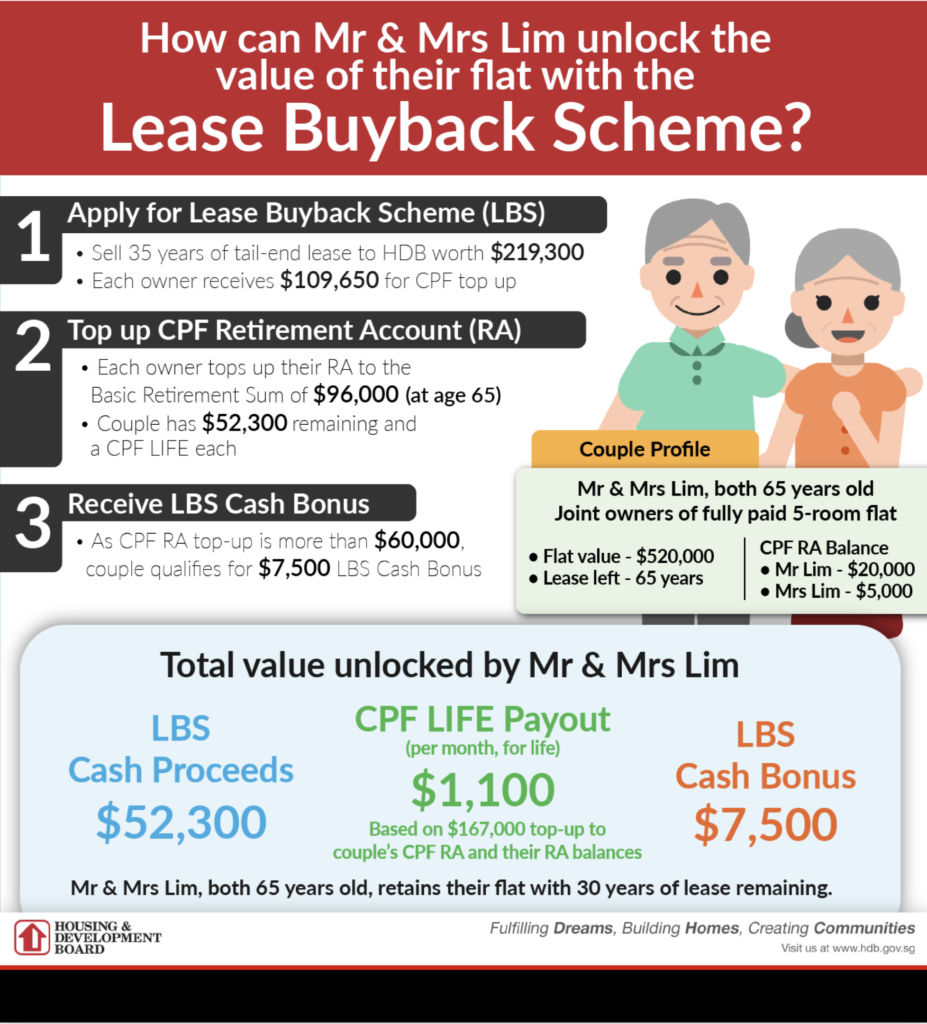

How do they then Unlock Capital in their HDB so they can get back to living their golden years comfortably?

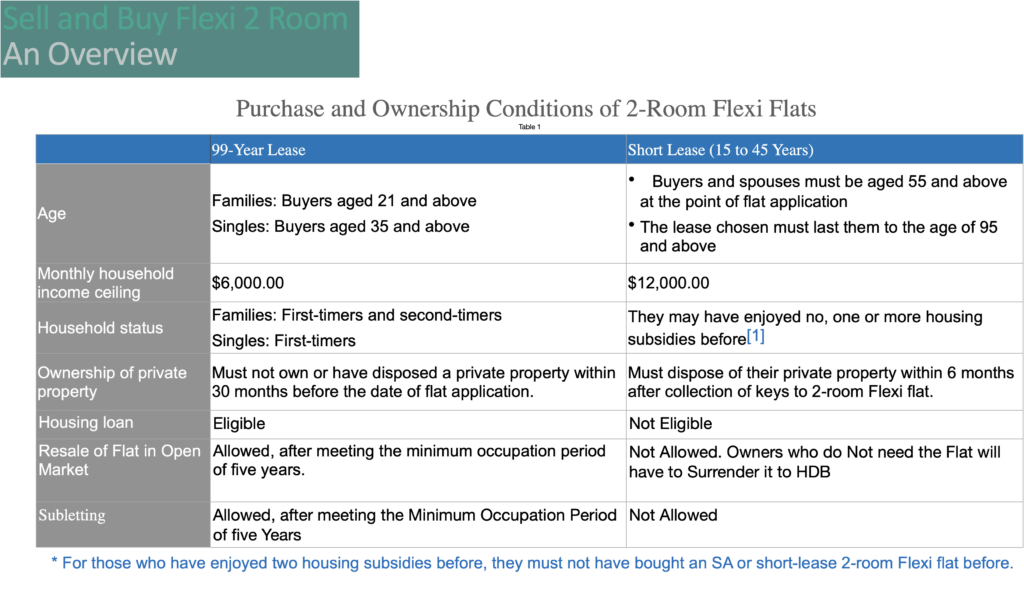

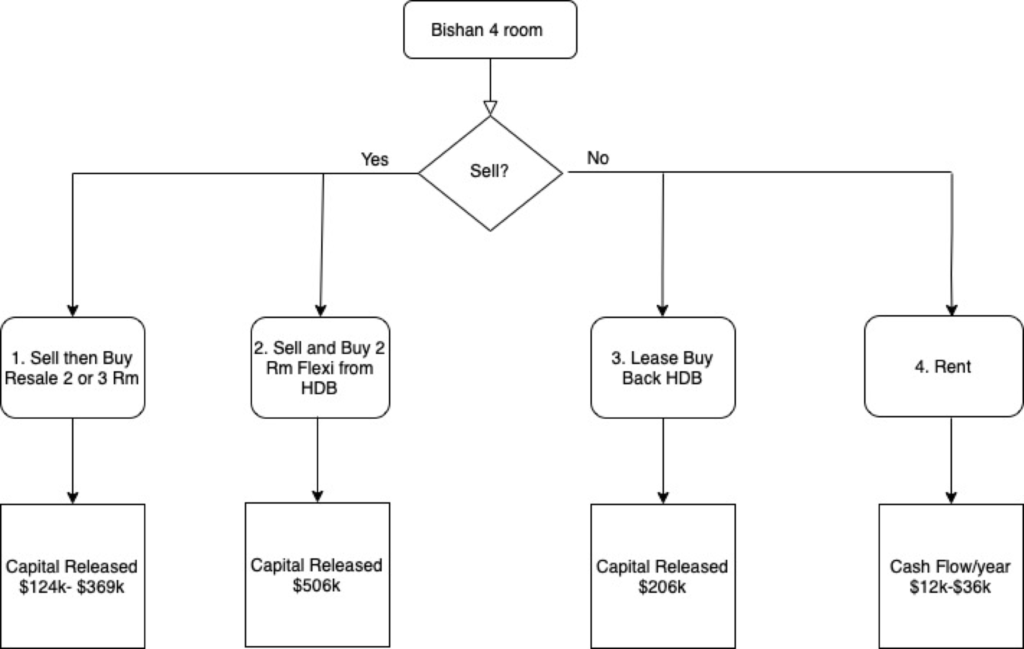

2. Selling And Buying A 2-Room Flexi HDB

If you are 70 yrs old, you can buy a 2 Room Flexi but you need to buy a minimum lease of 25 year or up to a minimum age of 95. Depending on the area you buy the 2 Room, whether it be in Matured estates or a newer one, it does offer a much less expensive option.

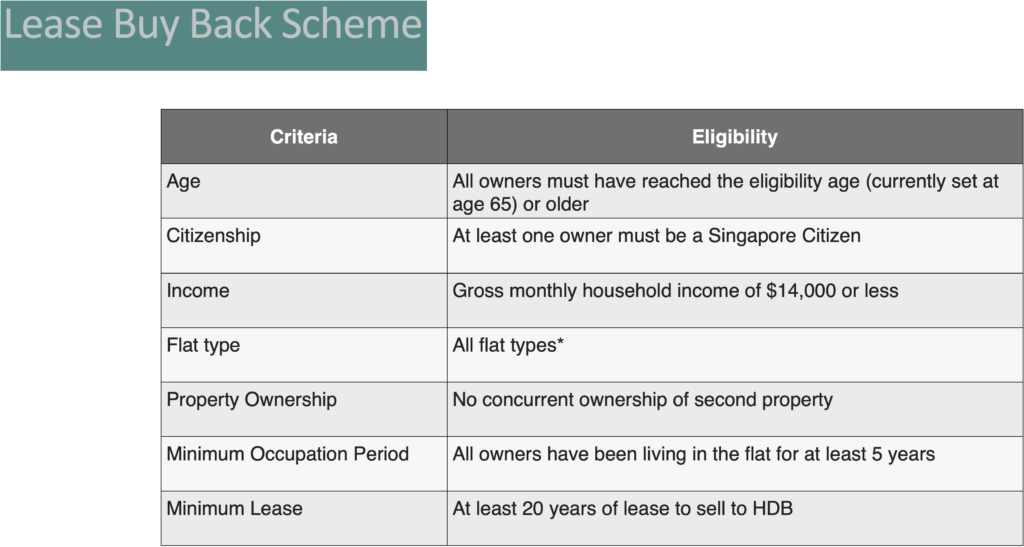

Here’s a summary of some of the conditions.

{kind=link}

Charlie Giang

A long time entrepreneur at large and Splitting his time between Silicon Valley and Singapore, Charlie’s not only familiar with investments in technology but has been an active investor in real estate in both countries.

Taking his unique background, he gives insights into real estate quite unlike another. A different and perhaps fresh perspective investing in Singapore’s real estate.

Get in touch with Charlie today.

You may also like...

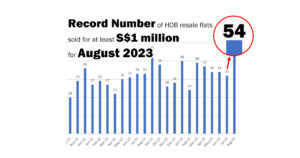

August Shatters Records: 54 HDBs Sold for Over a Million Each!

August Shatters Records: 54 HDBs Sold for Over a Million Each!

Decoding The Arden: Unveiling Potential Surprises Along the Way

Decoding The Arden: Unveiling Potential Surprises Along the Way

Proceed with Caution: Unveiling TMW Maxwell – Navigating Investment Prospects in District 2

Proceed with Caution: Unveiling TMW Maxwell – Navigating Investment Prospects in District 2

Hungry Ghost Festival: Does It Truly Spook Buyers in the Property Market?

Hungry Ghost Festival: Does It Truly Spook Buyers in the Property Market?

New Low for Weekend Launch on Aug 12-13, 2023

New Low for Weekend Launch on Aug 12-13, 2023

Enjoy what you have been reading? Join our mailing to get valuable insights delivered to your inbox today.

Appreciate to receive latest news estate planning.